The Evolving World of Gold-Backed Investments

For centuries, gold has represented wealth, security, and trust. It has survived wars, recessions, and market collapses — a timeless store of value when paper assets fail. In today’s uncertain financial landscape, investors are seeking ways to combine the stability of gold with the returns of modern investments.

That’s where gold bonds come in. Unlike physical gold, gold bonds let investors earn interest on their holdings — turning an idle asset into a source of passive income. They offer the dual benefit of capital appreciation from rising gold prices and fixed or compounding returns over time.

Among the various options available, Compound Gold Bonds (CGB) stand out for accredited investors seeking premium, gold-backed income opportunities. CGB merges the stability of physical gold with daily compounding interest and first-loss protection, offering a smarter and more rewarding way to grow wealth.

In this blog, we’ll explore how interest and redemption work in gold bonds, and how investors can make the most of their returns while preserving their capital.

Understanding Gold Bonds: A Quick Refresher

Gold bonds are financial instruments that allow investors to earn returns without having to physically hold or store gold. Instead, these bonds represent ownership of gold-backed assets held securely by the issuer.

What Are Gold Bonds?

A gold bond is typically denominated in units linked to gold (e.g., grams or ounces). When you invest in a gold bond, you are essentially lending money to the issuer, who guarantees to pay you periodic interest and redeem the bond’s value based on the prevailing price of gold at maturity.

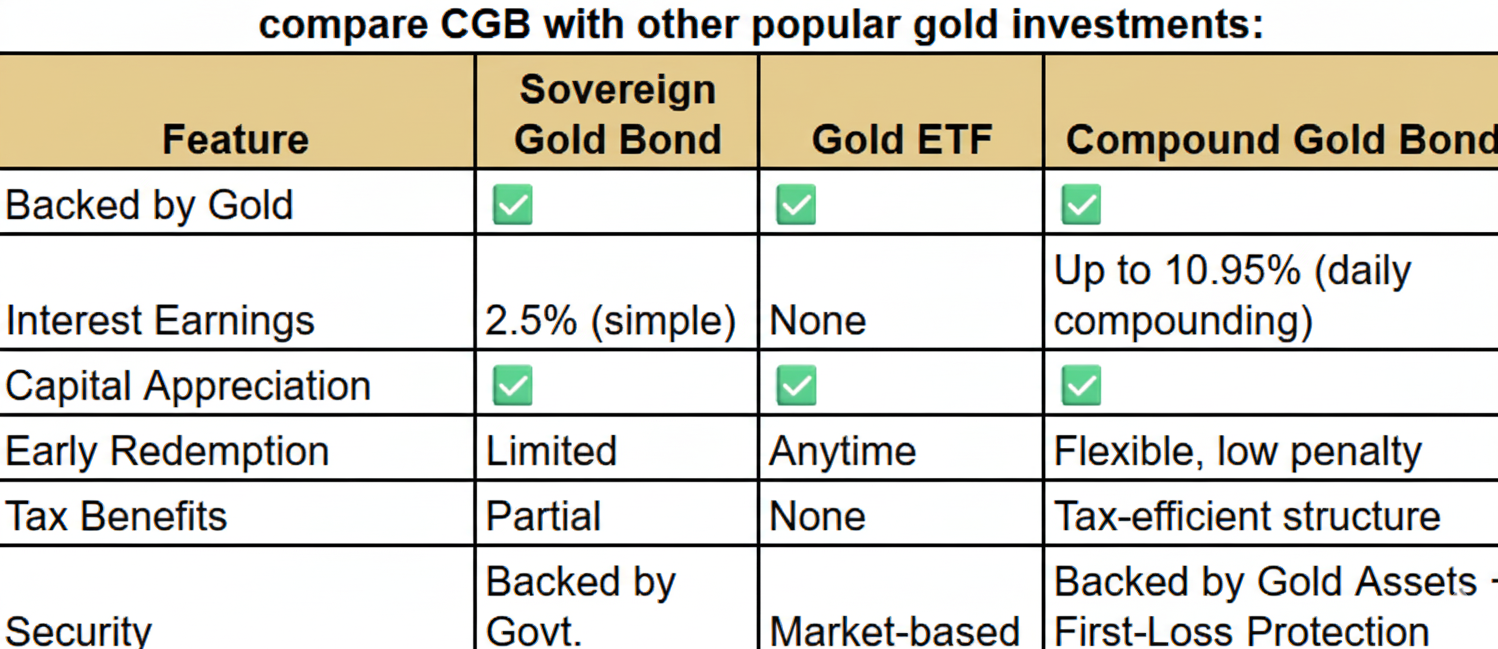

How Gold Bonds Differ from Other Gold Investments

Image

Gold bonds blend the security of gold with steady income generation, making them an attractive choice for investors seeking diversification and stability.

How Interest in Gold Bonds Works

The key advantage of gold bonds over physical gold is interest — your gold works for you while retaining its intrinsic value.

The Structure of Interest Payments

In traditional sovereign gold bonds, the government offers a fixed interest rate, usually around 2.5% per annum, paid semi-annually. This rate is earned in addition to any appreciation in the gold price.

However, modern private issuers like Compound Gold Bonds offer far more lucrative structures — with interest rates up to 10.95% APY, and daily compounding returns that grow faster than conventional interest models.

Interest in CGB is accrued daily and compounded automatically, meaning every day your earnings generate more earnings — a true formula for accelerated wealth creation.

The Power of Compounding in Gold Bonds

Compounding is the process where interest is added to the principal, so that future interest is calculated on the new, larger amount. Over time, this creates exponential growth.

For example:

If you invest $10,000 at 10.95% APY with daily compounding, after one year, your investment grows to approximately $11,151, compared to just $10,995 with simple interest.

The longer your tenure, the greater the compounding effect. Over 5 years, that same $10,000 would grow to nearly $17,000 under daily compounding — showcasing the real power of time and reinvestment.

CGB’s Unique Interest Model

Compound Gold Bonds take compounding to the next level with a daily yield accumulation system. Here’s what makes it unique:

- Daily Compounding: Interest accrues every single day, maximizing growth.

- No Hidden Fees: Investors enjoy full returns without deductions or commissions.

- Backed by Real Gold Assets: Interest is secured by gold-backed portfolios, ensuring safety.

- Stable, Predictable Growth: Returns are unaffected by market volatility or price manipulation.

This makes CGB an excellent choice for accredited investors seeking consistent income and long-term capital appreciation.

How Redemption in Gold Bonds Works

Interest is only one side of the equation. To fully understand gold bonds, investors must also grasp how redemption works — the process of converting bonds into cash or gold after maturity.

What Is Redemption?

Redemption is the act of receiving the maturity value of your bond — usually in cash equivalent to the current gold price, plus any accumulated interest.

For example, if you invest when gold is $2,000/oz and redeem when it’s $2,400/oz, your redemption value reflects both the price increase and the compounded interest earned.

Most gold bonds have a fixed tenure, such as 5 to 8 years, though some programs (like CGB) offer flexible redemption options.

Modes of Redemption

There are typically two ways gold bonds can be redeemed:

- Cash Redemption: Investors receive the cash equivalent based on the prevailing market price of gold.

- Gold Equivalent Redemption: Some issuers, including CGB, may allow investors to redeem in physical or allocated gold value.

Either way, the redemption amount = Principal + Accrued Interest + Capital Appreciation (if applicable).

Redemption Value Linked to Gold Prices

The redemption value of a gold bond is directly tied to gold’s market price on the redemption date. As gold prices rise, the value of your bond increases proportionally.

This gives investors a built-in hedge against inflation and currency depreciation. When markets falter and currencies weaken, gold prices typically rise — helping safeguard your investment’s real value.

For instance:

- You invest $10,000 when gold is $2,000/oz.

- After 5 years, gold rises to $2,500/oz (+25%).

- Your redemption value now reflects this increase, plus compounded returns.

This dual-benefit nature makes gold bonds an ideal mix of income and capital protection.

Early Redemption Options

Sometimes, investors need liquidity before maturity. Most sovereign bonds allow redemption after a lock-in period (usually 5 years) with certain conditions.

However, Compound Gold Bonds offer simplified early redemption structures, allowing partial or full exits with minimal penalties. Because the bonds are backed by liquid gold assets, investors enjoy flexibility and easy access to funds — without compromising returns.

Taxation of Interest and Redemption in Gold Bonds

Taxation plays an important role in the net returns investors receive.

- Interest Income: In most cases, the interest earned on gold bonds is treated as taxable income under “Income from Other Sources.”

- Capital Gains: Profits from redemption or sale depend on the holding period:

- Short-Term Capital Gains (STCG): If held for less than 3 years, gains are added to taxable income.

- Long-Term Capital Gains (LTCG): If held for 3 years or more, gains may be taxed at reduced rates, often with indexation benefits.

- Short-Term Capital Gains (STCG): If held for less than 3 years, gains are added to taxable income.

- Tax-Free Redemption (SGBs): Sovereign Gold Bonds offer exemptions on capital gains at maturity.

Compound Gold Bonds, depending on their structure, may provide tax-efficient returns, since interest is compounded and can be structured for optimized payout schedules.

Investors are advised to consult a tax professional to understand how their individual situation aligns with bond-specific benefits.

Example Scenarios: How Returns Add Up Over Time

Scenario 1: Traditional Gold Bond (Simple Interest)

- Investment: $10,000

- Interest Rate: 2.5% simple interest

- Tenure: 8 years

- Gold price increase: 20%

Final value:

$10,000 + (2.5% × 8 × $10,000) + 20% price gain = $13,000

Scenario 2: Compound Gold Bonds (Daily Compounding)

- Investment: $10,000

- Interest Rate: 10.95% APY

- Compounding: Daily

- Tenure: 5 years

Final value ≈ $17,000 — nearly 70% higher than the traditional bond.

Scenario 3: Early Redemption Simulation

- Investment: $50,000

- Duration: 2 years

- Daily compounding return: 10.95% APY

After 2 years, value ≈ $61,600.

Even with early redemption, the investor enjoys significant growth with minimal deductions — a major advantage of CGB’s flexible model.

Key Factors Affecting Interest and Redemption Outcomes

Your final returns from gold bonds depend on several factors:

- Gold Price Movements: Rising gold prices directly boost redemption value.

- Investment Tenure: The longer the compounding period, the higher the cumulative return.

- Interest Rate and Frequency: Daily compounding outperforms annual or semi-annual interest.

- Issuer Policies: Terms vary between sovereign and private issuers.

- Redemption Timing: Strategic redemption during high gold price phases maximizes profit.

For Compound Gold Bonds, these factors are optimized — offering high yield, flexibility, and gold-backed safety.

Why Compound Gold Bonds Stand Out

Let’s compare CGB with other popular gold investments:

CGB’s Unique Advantages

- Up to 10.95% APY — far higher than any traditional gold bond.

- Daily Compounding — your money grows every day.

- Gold-Backed Stability — physical and digital gold assets ensure safety.

- First-Loss Protection — added capital security layer for accredited investors.

- No Fees or Deductions — full transparency and direct investor benefit.

CGB transforms a passive gold holding into an active wealth-building instrument, combining yield, safety, and liquidity in one investment.

How to Invest and Redeem with CGB

Investing in Compound Gold Bonds is designed to be seamless and transparent. Here’s the step-by-step process:

- Eligibility Verification: CGB is available exclusively for accredited investors seeking high-yield, secure opportunities.

- Select Investment Amount: Choose your principal — starting at eligible minimum thresholds.

- Start Earning Daily Interest: Once invested, interest begins compounding daily, reflected in your investor dashboard.

- Monitor Growth: View your portfolio performance in real time with transparent reporting.

- Redeem Anytime: Choose to redeem after your lock-in period or at maturity — receive funds in cash or equivalent gold value.

Every CGB investment is backed by gold assets, ensuring stability and redemption liquidity. The process is simple, reliable, and designed for maximum investor confidence.

Conclusion: Turning Gold into Growing Wealth

Gold has always been a symbol of security — but with gold bonds, it becomes a source of steady, compounding income. Understanding how interest and redemption work allows investors to make smarter, more informed financial decisions.

While traditional gold bonds offer moderate returns and long lock-ins, Compound Gold Bonds redefine the category — combining daily compounding interest, first-loss protection, and gold-backed stability for high-yield, low-volatility growth.

For accredited investors seeking the best of both worlds — security and superior returns — Compound Gold Bonds present a future-ready path toward wealth creation.

✨ Invest smart. Grow daily. Stay golden with Compound Gold Bonds.

.png)