For accredited investors, the balance between liquidity, yield, and security is critical. Locking all your capital into a single maturity term can mean missing out on flexibility — or worse, missing better rates down the road. On the other hand, holding too much in short-term instruments often sacrifices returns.

Enter laddering — an investment strategy that helps you maximize returns, smooth cash flow, and preserve access to liquidity. At Compound Gold Bonds™ (CGB), we’ve structured laddering into our gold-backed bonds so investors don’t have to choose between yield and flexibility.

By spreading investments across different maturities — 6, 12, and 18 months — you create a “rolling ladder” that delivers regular liquidity while keeping most of your portfolio in higher-yielding terms. In this article, we’ll explore what laddering is, how it works with CGB, why it matters, and how it can strengthen your portfolio strategy.

What is CGB Laddering?

Laddering is an investment technique where your funds are divided across bonds with staggered maturities. Instead of locking your entire investment into a single term (say, 18 months), you split it into shorter and longer terms.

At CGB, laddering is designed around our three available maturities:

- 6-month bonds — offering short-term liquidity.

- 12-month bonds — balancing yield and flexibility.

- 18-month bonds — delivering the highest APY (up to 10.95%) for investors seeking maximum growth.

This approach ensures that every six months, part of your investment matures — giving you the choice to reinvest at new rates or withdraw cash if needed.

In other words, laddering creates a systematic rhythm of income and reinvestment, while reducing the risks of market timing.

How a CGB Ladder Works: A Step-by-Step Guide

Let’s walk through a simple example.

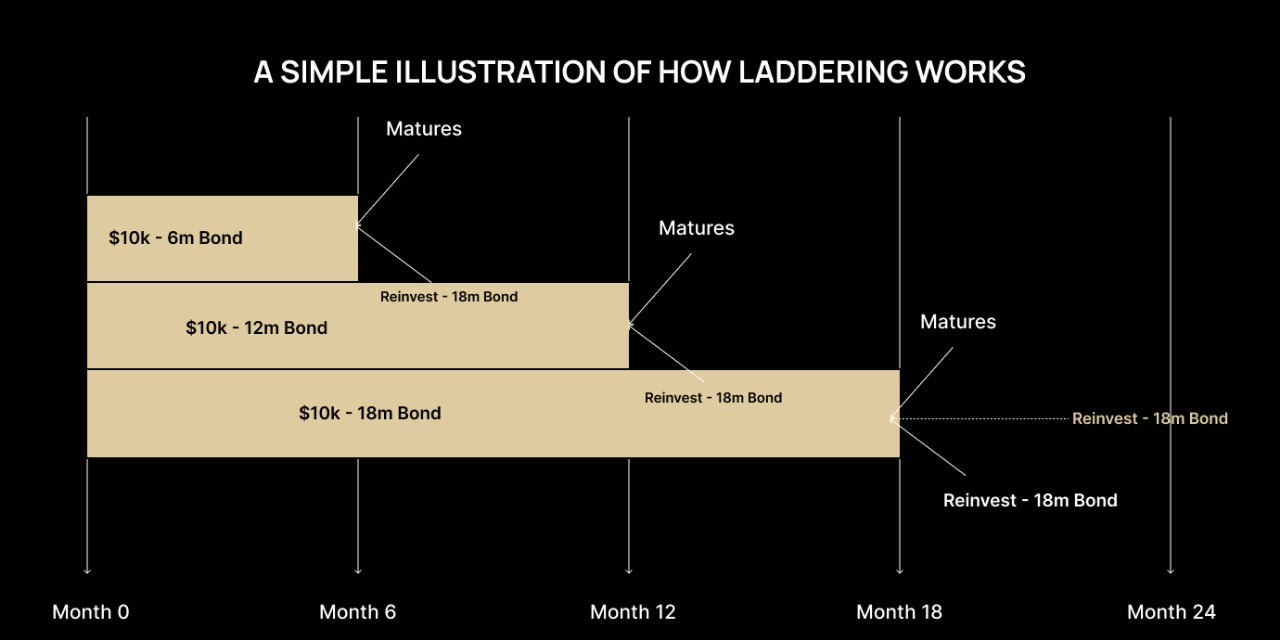

Imagine you invest $30,000 with CGB. Instead of placing it all into one maturity, you ladder it like this:

- $10,000 in a 6-month bond

- $10,000 in a 12-month bond

- $10,000 in an 18-month bond

Here’s what happens:

- At 6 months

- Your first $10,000 bond matures.

- You can either withdraw the funds or roll them into a new 18-month bond at the current APY.

- Meanwhile, your 12- and 18-month bonds continue compounding.

- At 12 months

- Your second $10,000 bond matures.

- Again, you can reinvest or take liquidity.

- By now, your reinvested 6-month bond has 12 months left on its ladder, and your original 18-month bond has 6 months remaining.

- Your second $10,000 bond matures.

- At 18 months

- Your third $10,000 bond matures.

- The cycle continues — you now have a rolling ladder, with one bond maturing every six months.

- Your third $10,000 bond matures.

CGB Laddering Diagram

Here’s a simple illustration of how laddering works:

This creates a perpetual cycle of maturities, ensuring you always have access to liquidity while maximizing compounding.

The Key Benefits of CGB Laddering

1. Regular Liquidity

One of the most practical advantages of CGB laddering is that you are never entirely locked out of your investment. Every six months, a portion of your funds matures and becomes available to you. This regular liquidity is especially valuable for investors who want predictable access to cash without disrupting their entire portfolio. Unlike traditional long-term bonds — which often require you to wait years before accessing principal — laddering provides a steady rhythm of returns, allowing you to balance security with short-term flexibility.

2. Better Yield Capture

Interest rates are never static. They move with inflation, monetary policy, and global economic conditions. Laddering positions you to take advantage of these changes. When a bond matures, you can reinvest it at the prevailing APY, which may be higher than when you initially invested. With CGB, this could mean capturing yields of up to 10.95% APY on reinvestment. Instead of being stuck with yesterday’s rates, laddering ensures your portfolio can adapt to today’s opportunities.

3. Diversified Timing

Timing the market — or locking all of your funds into one rate environment — carries unnecessary risk. With CGB laddering, your investment maturities are staggered across 6-, 12-, and 18-month terms. This diversification smooths out timing risk, ensuring you’re not overly exposed to a single economic cycle or interest-rate environment. By spreading your exposure across maturities, you build resilience into your portfolio and reduce the impact of market fluctuations.

4. Compounding Power

The true engine of long-term wealth growth is compounding. Every time a bond matures and you reinvest the principal plus accrued interest, your base investment grows larger. With CGB’s daily compounding returns, this effect is amplified. Over time, the reinvested earnings generate their own returns, creating a snowball effect. This means that laddering not only gives you liquidity but also systematically strengthens your earning power year after year.

5. Flexibility and Control

Perhaps the most underrated benefit of CGB laddering is the control it gives you as an investor. At each maturity date, you are in the driver’s seat: you can choose to reinvest into a higher-yielding 18-month bond, or you can withdraw funds to cover personal or business needs. This decision-making flexibility ensures that your investment strategy evolves with your financial goals. You’re never forced into a rigid structure — instead, you retain the ability to adapt as your circumstances change.

Why Laddering Matters for Investors

For accredited investors, one of the greatest challenges is finding the right balance between yield, safety, and access. Most traditional investments force compromises:

- Stocks: Offer strong growth potential but come with high volatility and can be difficult to liquidate in a down market.

- Real estate: Provides tangible, income-generating assets but often requires long holding periods and large capital commitments.

- Certificates of Deposit (CDs): Safe and predictable, but rigid, with fixed rates and penalties for early withdrawals.

CGB laddering offers a middle ground. With bonds backed by gold, you gain a tangible and inflation-resistant foundation. The yields — up to 10.95% APY — are competitive with riskier asset classes, while rolling maturities ensure you have liquidity and reinvestment opportunities every six months. In a market shaped by shifting interest rates, inflation, and volatility, laddering helps keep your portfolio adaptable.

Real-Life Application

Consider two different investor profiles:

- Investor A: Prefers Liquidity

Laddering ensures that every six months, Investor A has funds available. If unexpected expenses arise, they can take cash instead of reinvesting, without disrupting their entire portfolio. - Investor B: Maximizes Growth

Investor B reinvests every maturing bond into a new 18-month term. Over time, their portfolio steadily shifts into higher-yielding bonds while compounding daily, accelerating long-term growth.

In both cases, laddering adjusts to the investor’s goals — offering flexibility for conservative investors and powerful growth potential for those seeking higher returns.

Why Choose CGB for Laddering

Not all bond strategies are created equal. Here’s what sets CGB laddering apart:

- Backed by Gold → a historically resilient, inflation-resistant asset.

- Up to 10.95% APY → among the most attractive yields available in secured bond investments.

- Daily Compounding → every reinvestment maximizes your returns.

- First-Loss Protection → providing an additional layer of security for your capital.

- No Fees → ensuring every dollar is working for you.

By combining gold-backed security with high-yield terms and flexible reinvestment options, CGB laddering gives accredited investors a unique and strategic way to build wealth with confidence.

Conclusion

Laddering is more than just a clever investment tactic — it’s a disciplined approach to balancing yield, liquidity, and growth.

With Compound Gold Bonds™ laddering, you gain:

- Regular access to liquidity every 6 months.

- The ability to capture higher rates as markets shift.

- Compounding power that accelerates wealth-building.

- Gold-backed security and first-loss protection.

Whether you’re seeking dependable cash flow, inflation-hedged stability, or long-term growth, CGB laddering offers a premium solution tailored for accredited investors.

In uncertain times, strategies like laddering provide not just higher returns — but also peace of mind. With CGB, you don’t just invest in bonds. You build a resilient, flexible ladder toward lasting financial success.

Frequently Asked Questions

1. What is the minimum amount I need to start CGB laddering?

To build a proper ladder, we recommend spreading your investment evenly across 6-, 12-, and 18-month bonds. A common starting example is $30,000, split into three allocations of $10,000 each. However, accredited investors may start with higher or lower amounts depending on their financial goals. The key is to divide your capital across different maturities so you can benefit from regular liquidity and reinvestment opportunities.

2. How is laddering different from just investing in a single long-term bond?

When you invest in a single long-term bond, your funds are locked until maturity — which can limit liquidity and prevent you from capturing higher yields if interest rates rise. With laddering, you split your investment across multiple maturities. This creates rolling access to your funds every six months, while still keeping most of your portfolio in higher-yielding terms. In short, laddering balances flexibility with growth, whereas a single bond sacrifices one for the other.

3. Is CGB laddering suitable for short-term investors?

Yes — laddering can work for both short- and long-term strategies. If you prefer liquidity, you can use the 6-month maturity as a way to keep part of your portfolio accessible while still earning competitive yields. For longer-term investors, reinvesting maturing bonds into new 18-month terms compounds returns and steadily shifts more of the portfolio into the highest APYs. This makes laddering versatile enough to adapt to different investment horizons.

4. Are my returns guaranteed with CGB laddering?

CGB bonds offer fixed, contractually locked-in APYs of up to 10.95%, depending on the term you choose. Once you invest, your rate does not change for the life of that bond. The laddering strategy simply determines how your funds are allocated and reinvested over time. Additionally, all CGB bonds are backed by gold assets and include first-loss protection, adding layers of security not found in many traditional investments.

5. Can I customize my ladder with different amounts?

Absolutely. While the standard example uses equal allocations (e.g., $10,000 per term), you can customize your ladder based on your priorities. For instance:

- If you want more liquidity, you can allocate a larger portion to 6-month bonds.

- If you want maximum yield, you can weight more toward 18-month bonds.

- If you want balance, you can spread evenly across all terms.

CGB laddering is designed to be flexible, giving accredited investors control over how their funds are distributed across maturities.

.png)