For generations, gold has been a cornerstone of wealth preservation. In uncertain economic times, investors often turn to this precious metal for stability, protection against inflation, and long-term security. For U.S. investors planning their retirement, two of the most talked-about gold-based options are Gold IRAs and Gold Bonds.

But which one is the smarter choice for retirement planning in 2025 and beyond?

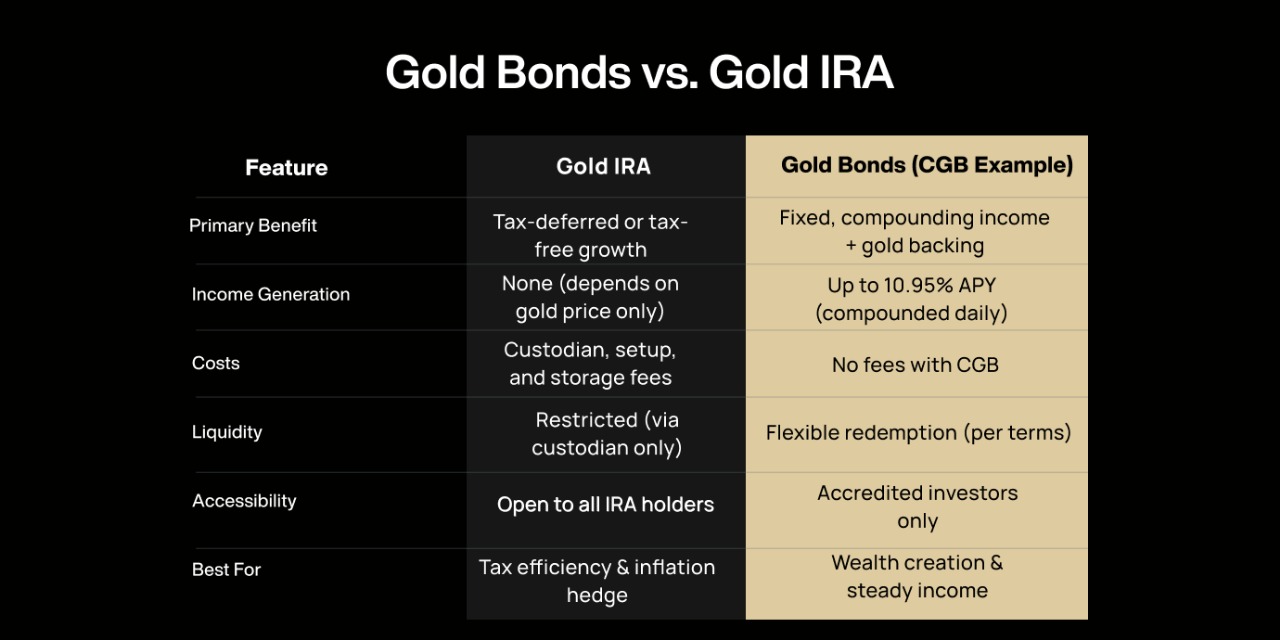

Both offer exposure to gold, but they work in very different ways. A Gold IRA is a tax-advantaged retirement account holding physical gold, while Gold Bonds—like Compound Gold Bonds™ (CGB)—provide gold-backed security along with fixed, compounding income. Understanding the strengths and limitations of each is essential if you want your retirement strategy to deliver both security and growth.

What is a Gold IRA?

A Gold IRA is a self-directed Individual Retirement Account (IRA) that allows investors to hold physical gold and other approved precious metals instead of traditional assets like stocks and bonds.

Key Features:

- Holds IRS-approved gold coins and bullion.

- Requires a custodian and an approved depository for storage.

- Offers the same tax benefits as traditional or Roth IRAs (tax-deferred growth or tax-free withdrawals, depending on the type).

Why Investors Choose Gold IRAs:

- Long-term hedge against inflation.

- Portfolio diversification.

- Tangible asset ownership inside a retirement account.

However, while the idea of owning gold in your retirement portfolio sounds appealing, there are significant downsides that investors should weigh carefully.

What are Gold Bonds?

Gold Bonds are investment products backed by physical gold reserves but structured to deliver fixed income over a set period. Unlike physical gold or Gold IRAs, which depend solely on price appreciation, gold bonds generate predictable returns.

For example, Compound Gold Bonds™ offer:

- Up to 10.95% APY with daily compounding.

- No fees (unlike Gold IRAs that charge custodial and storage fees).

- First-loss protection, ensuring greater security for investors.

- Exclusivity: Available only to U.S. accredited investors.

This makes Gold Bonds, particularly CGB, more than just a hedge—they’re an income-generating vehicle designed for long-term wealth creation.

To learn how to build wealth with gold, read Gold Bonds for Long-Term Wealth Creation.

Gold IRA – Pros and Cons

Pros of a Gold IRA:

- Tax Advantages – Contributions to a traditional Gold IRA are tax-deductible; Roth IRAs allow tax-free withdrawals.

- Inflation Hedge – Gold typically retains value in times of economic turmoil.

- Diversification – Adds balance to portfolios heavily weighted in stocks and bonds.

- Long-Term Wealth Preservation – Ideal for investors who want to hold physical gold for decades.

Cons of a Gold IRA:

- High Fees – Custodian, setup, and storage fees eat into returns

- No Income – Gold inside an IRA doesn’t generate dividends or interest.

- Complex Regulations – Strict IRS rules on what type of gold qualifies, where it must be stored, and how it’s managed.

- Liquidity Issues – Selling requires going through custodians, which can be slow and costly.

In short: A Gold IRA works well if your priority is tax efficiency and inflation hedging, but it offers no predictable income stream.

Gold Bonds – Pros and Cons

Pros of Gold Bonds:

- Fixed, Predictable Income – Regular interest payments plus exposure to gold’s value.

- Compounding Growth – Returns increase over time, especially with products like CGB offering daily compounding.

- No Storage Hassle – Unlike Gold IRAs, there’s no need for vaults or custodians.

- Liquidity – Bonds can often be redeemed more flexibly than IRA gold.

- No Fees – Premium products like Compound Gold Bonds™ eliminate hidden costs.

Cons of Gold Bonds:

- No IRA Tax Deferrals – Returns are taxable in the year earned.

- Eligibility Restrictions – Many high-yield options, including CGB, are limited to accredited investors.

In short: Gold Bonds are ideal for investors seeking reliable returns and growth, without the complexity of retirement account regulations.

Gold Bonds vs. Gold IRA: Head-to-Head Comparison

Which One is Better for Retirement Planning?

The answer depends on your personal retirement goals:

- If your priority is tax efficiency and inflation hedging, a Gold IRA can be a solid addition to your retirement portfolio. However, you must be prepared for higher fees, limited liquidity, and zero income generation.

- If you value predictable income, compounding growth, and simplicity, Gold Bonds—especially Compound Gold Bonds™—are the superior choice. They not only protect wealth with gold backing but also grow it with fixed high yields, making them ideal for long-term retirement planning.

- For many investors, the best solution may be a combination: using Gold IRAs for tax-deferred protection and Gold Bonds for steady cash flow.

Practical Considerations Before Choosing

When deciding between a Gold IRA and Gold Bonds, it’s essential to take your personal financial situation and long-term goals into account. One of the first factors is your time horizon. If you are still decades away from retirement, you may be comfortable locking funds into a Gold IRA for the long term, focusing on tax efficiency and preservation. On the other hand, if you are closer to retirement or already planning withdrawals, the consistent cash flow and flexibility of Gold Bonds may serve you better.

Another important factor is risk tolerance. Some investors are comfortable with the fluctuations in gold’s market price, understanding that their Gold IRA may rise or fall in value depending on external conditions. Others prefer the stability of fixed, guaranteed returns, which makes Gold Bonds—particularly products like Compound Gold Bonds™—a more appealing choice.

Your income needs also play a critical role. If your strategy is to generate passive income that supplements your lifestyle today or in retirement, Gold Bonds provide steady interest payouts that can grow over time with compounding. By contrast, Gold IRAs are designed primarily for wealth preservation and tax-advantaged growth rather than immediate income generation.

The tax situation is another key consideration. Investors who benefit from tax-deferred contributions or tax-free withdrawals may find Gold IRAs attractive, especially for long-term retirement planning. However, while Gold Bonds do not carry IRA-style tax benefits, their higher yields can often outweigh those advantages.

Finally, there is the matter of accreditation. Gold IRAs are broadly accessible to anyone with retirement savings, but high-yield products like Compound Gold Bonds™ are exclusive to accredited investors. If you meet the criteria, you gain access to institutional-grade opportunities with stronger yields, daily compounding, and first-loss protection—advantages that traditional Gold IRAs simply cannot match.

Conclusion

Both Gold IRAs and Gold Bonds play a role in retirement planning, but they serve different purposes. Gold IRAs help with tax efficiency and wealth preservation, while Gold Bonds stand out as a high-yield, gold-backed solution that builds wealth through compounding interest.

For accredited U.S. investors seeking elite, premium retirement investments, Compound Gold Bonds™ provide up to 10.95% APY, no fees, and strong protection—making them a superior option for those who want their gold to work harder for their retirement.

FAQs

1. Can I hold gold bonds inside a Gold IRA?

No. Gold IRAs are designed to hold physical gold or approved precious metals. Bonds like CGB are separate investment products and cannot be placed directly inside an IRA.

2. Which has higher returns: Gold Bonds or Gold IRA?

Gold Bonds typically offer higher, fixed returns (up to 10.95% APY with CGB), whereas Gold IRA returns rely solely on gold price appreciation and may be offset by fees.

3. Are Gold Bonds risk-free?

No investment is completely risk-free, but CGB offers first-loss protection and gold-backed security, making it far more stable than speculative assets.

4. What tax benefits do I lose with Gold Bonds compared to a Gold IRA?

Gold IRA investments can grow tax-deferred or tax-free (depending on the account type). Gold Bonds generate taxable income annually, but their higher yields often outweigh tax disadvantages.

5. Is Compound Gold Bonds™ available to all U.S. investors?

No. CGB is exclusively available to accredited investors, ensuring it remains a premium, institutional-grade investment product.

6. Can I diversify by holding both?

Yes. Many investors use Gold IRAs for tax efficiency while adding Gold Bonds to generate predictable income and compounding growth.

.png)